Islamic Finance Options for Muslim Nonprofits CIC is currently inactive and is preparing to close. We will submit final accounts and apply for voluntary strike-off from the Companies Register shortly. This website will remain online for notification purposes only during the winding down process. For any enquiries, please contact: nasihah@ifomn.org. Thank you!

IFOMN's Somalia Nonprofit Banking Blueprint

IFOMN’’s flagship initiative, Somalia Nonprofit Banking Blueprint focuses on developing nonprofit bank products for Muslim Nonprofits, like current accounts, with Islamic Financial Institutions (IFIs) globally to address a dire need for such products and to tackle the nonprofit debanking crisis (see below) as part of the first cohort of the Cambridge Social Ventures Peaceshaping & Climate Incubator (2024-5):

IFOMN's initial findings show some AMAZING things:

Somalia has the highest concentration of Shariah-compliant (I)NGO, charity, and nonprofit accounts in the world!

Somalia is the only country where Islamic Financial Institutions (IFIs) have created dedicated Islamic nonprofit accounts!

These accounts represents a crucial learning opportunity for IFIs everywhere!

What is Debanking? How Does it Impact Muslim Nonprofits?

Debanking refers to the closure or restriction of banking services, often without clear explanation, due to perceived risks. For UK Muslim nonprofits, debanking is particularly problematic as it directly affects their ability to operate, erodes donor trust, delays aid delivery, and perpetuates financial exclusion. This issue often stems from systemic biases, regulatory pressures, and the operational challenges faced by banks in ensuring compliance with anti-money laundering (AML) and counter-terrorism financing (CTF) laws.

Why Do UK Banks De-Risk or Debank Muslim Nonprofits?

1. Regulatory Compliance and "De-Risking" Strategies

AML and CTF Laws:

Muslim nonprofits working in conflict zones or high-risk areas are flagged for heightened scrutiny due to fears of fund misuse. Banks face penalties under laws like the Proceeds of Crime Act for failing to detect financial crimes, prompting risk-averse behavior.Perceived High Risk:

Sending funds to politically unstable regions increases the likelihood of being labeled as high-risk, even without evidence of wrongdoing.

2. Cost of Compliance vs. Profitability

Resource-Intensive Monitoring:

Banks must perform extensive due diligence and monitoring on flagged accounts, particularly for international transfers, which is resource-heavy.Profit Margins:

Many Muslim nonprofits manage modest account balances and low-value transactions, making them less profitable compared to their compliance costs.

3. Reputation Management and Fear of Penalties

Reputation Risk:

Banks are wary of reputational damage if linked to organizations accused (fairly or unfairly) of financing terrorism.Large Fines:

Regulatory penalties for AML and CTF failures push banks to adopt cautious, sweeping measures like de-risking.

4. Biases and Systemic Discrimination

Implicit Bias:

Muslim nonprofits are often unfairly subjected to "guilt by association," with their Islamic identity or regional focus prompting undue suspicion.Media Narratives:

Negative portrayals in the media further amplify stigma and distrust, even when accusations are baseless.

5. Lack of Transparency in Banking Decisions

Unexplained Closures:

Many Muslim nonprofits report account closures without clear reasons, making it impossible to address perceived risks.No Tailored Solutions:

The absence of specialized banking products for faith-based nonprofits leaves Muslim charities more vulnerable to de-risking.

6. Influence of International Relations

US Policies:

US-led counter-terrorism measures often shape global banking practices, with heightened scrutiny on Muslim organizations.Sanctioned Regions:

Charitable work in sanctioned areas like Palestine and Syria raises red flags, even for legitimate humanitarian efforts.

Consequences of Debanking for Muslim Nonprofits

Financial Exclusion:

Nonprofits struggle to open or maintain accounts, hindering their ability to function effectively.Erosion of Donor Trust:

Account closures create doubts about legitimacy, discouraging potential donors.Delayed Aid Delivery:

Administrative roadblocks slow down critical aid to vulnerable communities.Systemic Inequality:

De-risking perpetuates financial barriers for Muslim-led organizations, limiting their societal contributions.

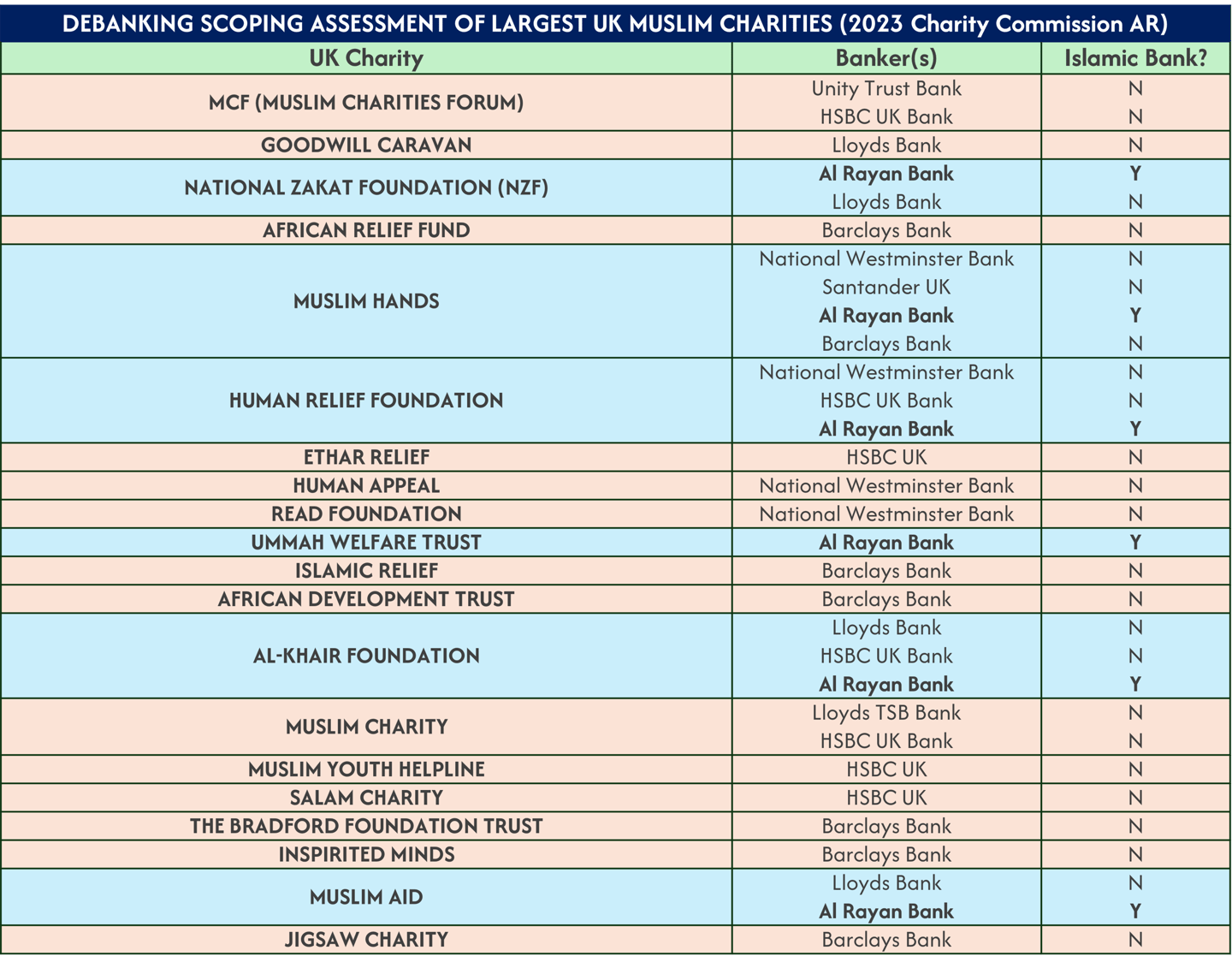

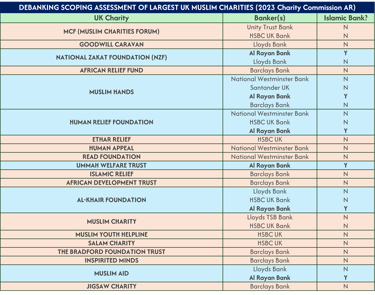

Surprising Stats from the UK

IFOMN's research of banker selection trends among UK Muslim charities as shown in their yearly Trustee reports submitted to the Charity Commission shows that 15 out of 20 of the most well-known UK Muslim charities don’t bank with Islamic banks.

This is not by choice but because of a lack of tailored Islamic nonprofit banking options in the Islamic finance sector. The UK is not alone in this.

The lack of accessible Islamic nonprofit banking solutions poses a significant barrier for Muslim charities in the UK.

Many Muslim charities are unable to align their banking practices with their faith, leaving them vulnerable to financial exclusion and potential debanking.

What Can Be Done?

1. Develop Tailored Nonprofit Banking Products

Dedicated Islamic financial solutions, such as Shariah-compliant nonprofit accounts, can address the unique needs of Muslim charities.

2. Strengthen Advocacy Efforts

Organizations like the Muslim Charities Forum (MCF) in the UK and other similar umbrella organisations abroad must continue to lead sector-wide campaigns for fair and transparent banking practices (https://www.muslimcharitiesforum.org.uk/2022/07/27/second-news-post/)

IFOMN joins this fight by addressing the sizable global gap in dedicated Islamic nonprofit banking options and looks to work with both IFIs and Muslim Nonprofits to make this a reality.

3. Foster Partnerships with Islamic Financial Institutions

Collaboration with IFIs can provide compliant and supportive banking options, reducing reliance on conventional banks.

We see this as the central way that the Muslim nonprofit sector can safeguard itself from debanking risk by joining forces with IFIs who are subject to many of the same systemic biases that lead conventional banks to debank Muslim nonprofits.

The Way Forward

Addressing debanking is essential for empowering Muslim nonprofits (charities and social enterprises alike).

By combining tailored financial solutions, advocacy, and partnerships, we can mitigate these challenges and ensure these organisations can continue their vital work without unnecessary financial or spiritual barriers.

This approach aligns with broader goals of inclusivity, capacity building, and sustainable growth in the Muslim nonprofit ummah globally!

Key Reading for Understanding Muslim Nonprofit Debanking in the UK

1. The Risk Advisory Group. (2015) 'Banks’ de-risking and the effect on Muslim charities', 1 July. Available at: https://www.riskadvisory.com/news/banks-de-risking-and-the-effect-on-muslim-charities/

This analysis explores the trend of banks de-risking by severing ties with clients perceived as high-risk, including Muslim charities. It discusses the unintended consequences of such policies, such as financial exclusion and operational challenges for legitimate charitable organizations. The report calls for a balanced approach to risk management that does not disproportionately impact specific communities.

2. Muslim Charities Forum. (2022). Confronting the Hurdles: How Banking Access Challenges are Disrupting Humanitarian Work. (https://www.muslimcharitiesforum.org.uk/2022/07/27/second-news-post/)

This article delves into the disproportionate effects of financial access challenges on Muslim-led and small charities. Fadi Itani, CEO of MCF, emphasizes the increasing difficulties within the financial landscape for these organizations and advocates for a comprehensive approach to address potential risks rather than broad avoidance.

3. Evening Standard. (2023) 'Call for review as "British Muslims disproportionately affected by de-banking"', 1 August. Available at: https://www.standard.co.uk/business/business-news/call-for-review-as-british-muslims-disproportionately-affected-by-debanking-b1098010.html

This news piece reports on calls from the Muslim Council of Britain for an impartial review into banking practices. It highlights concerns over the disproportionate impact of debanking on British Muslims and emphasizes the need for fair treatment and transparency from financial institutions.

4. Muslim Charities Forum. (2023). Farage De-risking Scandal Casts Spotlight on Long-running Issue for Muslim-led Charities. (https://www.civilsociety.co.uk/voices/fadi-itani-the-farage-de-risking-scandal-has-been-happening-to-muslim-charities-for-years.html)

This piece highlights the parallels between the high-profile de-risking incident involving Nigel Farage and the longstanding banking challenges faced by Muslim-led charities. It underscores the systemic nature of debanking within the sector and calls for sustained efforts to address these issues.

CHECK OUT NOW the Muslim Charities Forum recently released Debanking Report:

https://www.muslimcharitiesforum.org.uk/resources/the-landscape-of-debanking-within-muslim-charities-and-its-impact-on-charitable-activities/

© 2025. All rights reserved.

Islamic Finance Options for Muslim Nonprofits (IFOMN) is a Community Interest Company Limited by Guarantee Registered in England and Wales (Company No. 15920704). Office: 61 Bridge Street, Kington, United Kingdom, HR5 3DJ